")

")

COP26 resonates across the Caspian

With the uncertainty of the energy security situation, persistent shortage of natural gas in all segments of the world market against the background of the expected drive out of oil, coal and “peaceful” atom from European energy balances, the development of new large fields in the Caspian region is becoming increasingly topical.

There were more than 160 structures revealed in the Caspian Sea as early as in the 20th century, which may potentially contain up to 10 trillion cubic meters of natural gas hidden in hard-to-reach high-pressure formations, mainly in the deep waters of the Caspian Sea. Their development requires not only expensive and most-advanced environmentally friendly technologies, but also the well coordinated work of all the Caspian states in creating a favorable investment climate, which is more than possible after the signing of the Convention on the Caspian Sea status on August 12, 2018. The restoration of the territorial integrity of Azerbaijan, which is the central transport link of the so-called “Greater Caspian Region” stretching from India to the Black and Mediterranean Seas with the Caspian Sea in the center, has increased its role as a key platform for stability and security at the junction of Europe and Asia. All this attracts the attention of investors. The Caspian Sea has large proven reserves of natural gas, as well as a developed export infrastructure capable of increasing the maximum carrying capacity to 40-50 bcm per year from today’s 10 bcm.

Newly commissioned fields, as well as additional exploration and exploitation of previously identified promising areas, can support exports until 2050 when the EU will abandon fossil fuels.

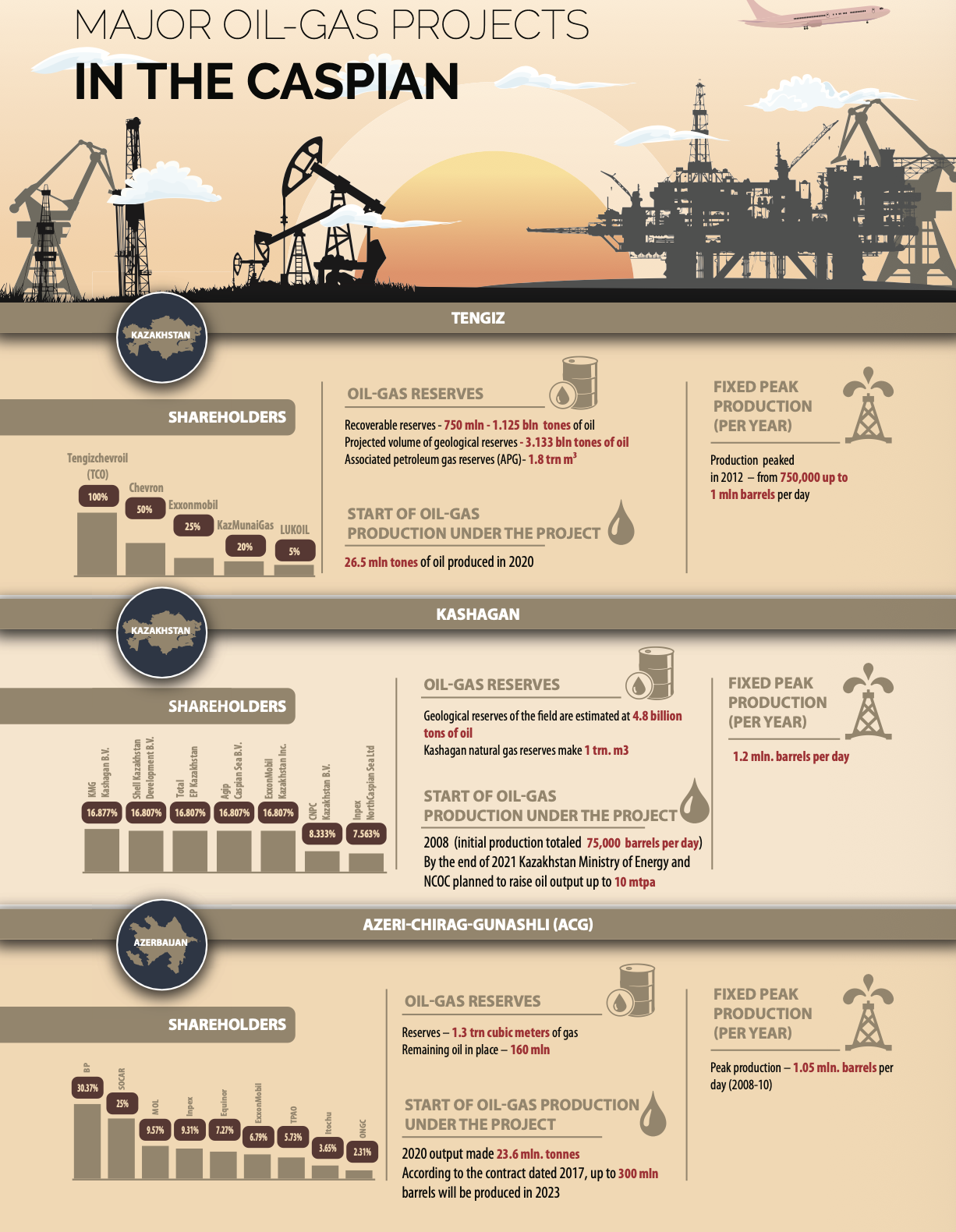

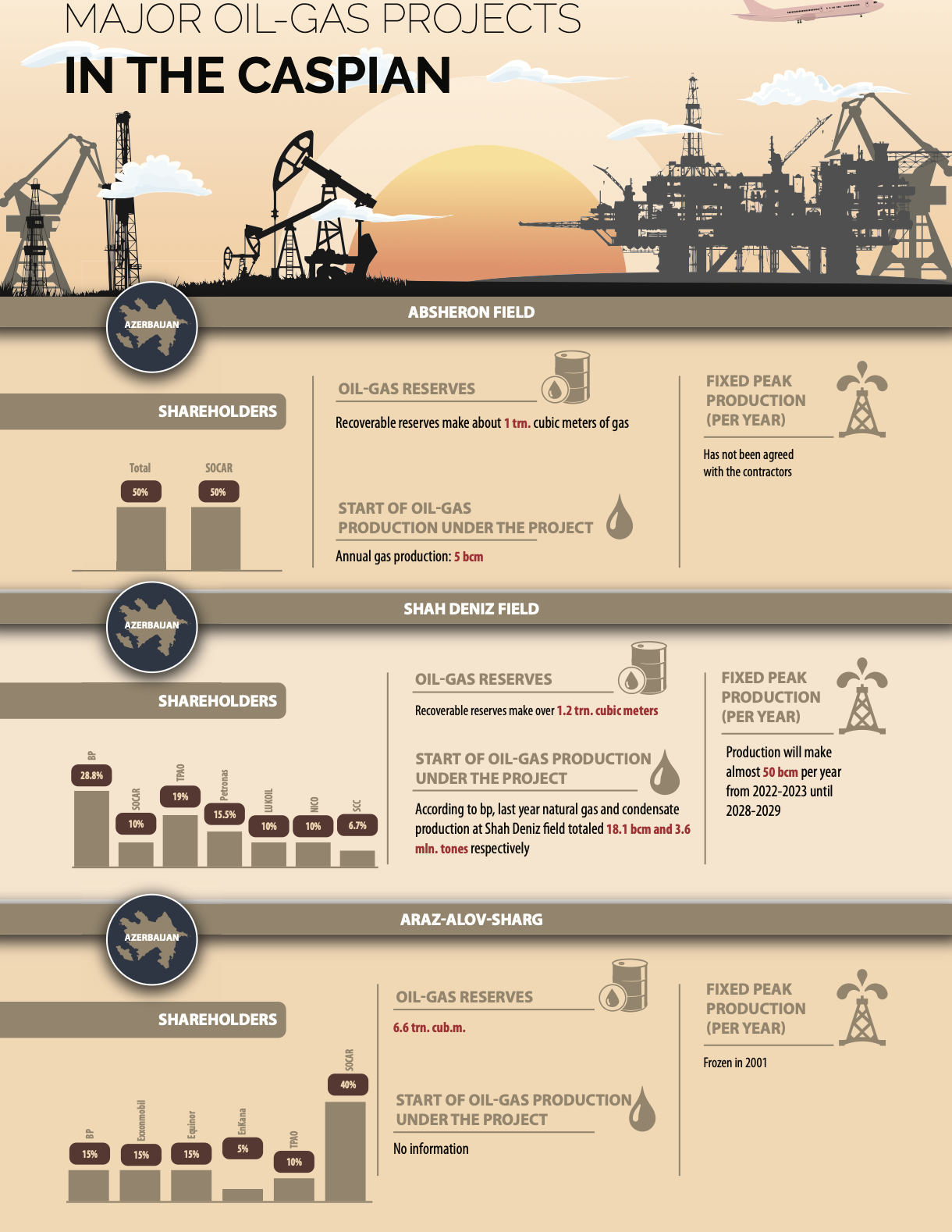

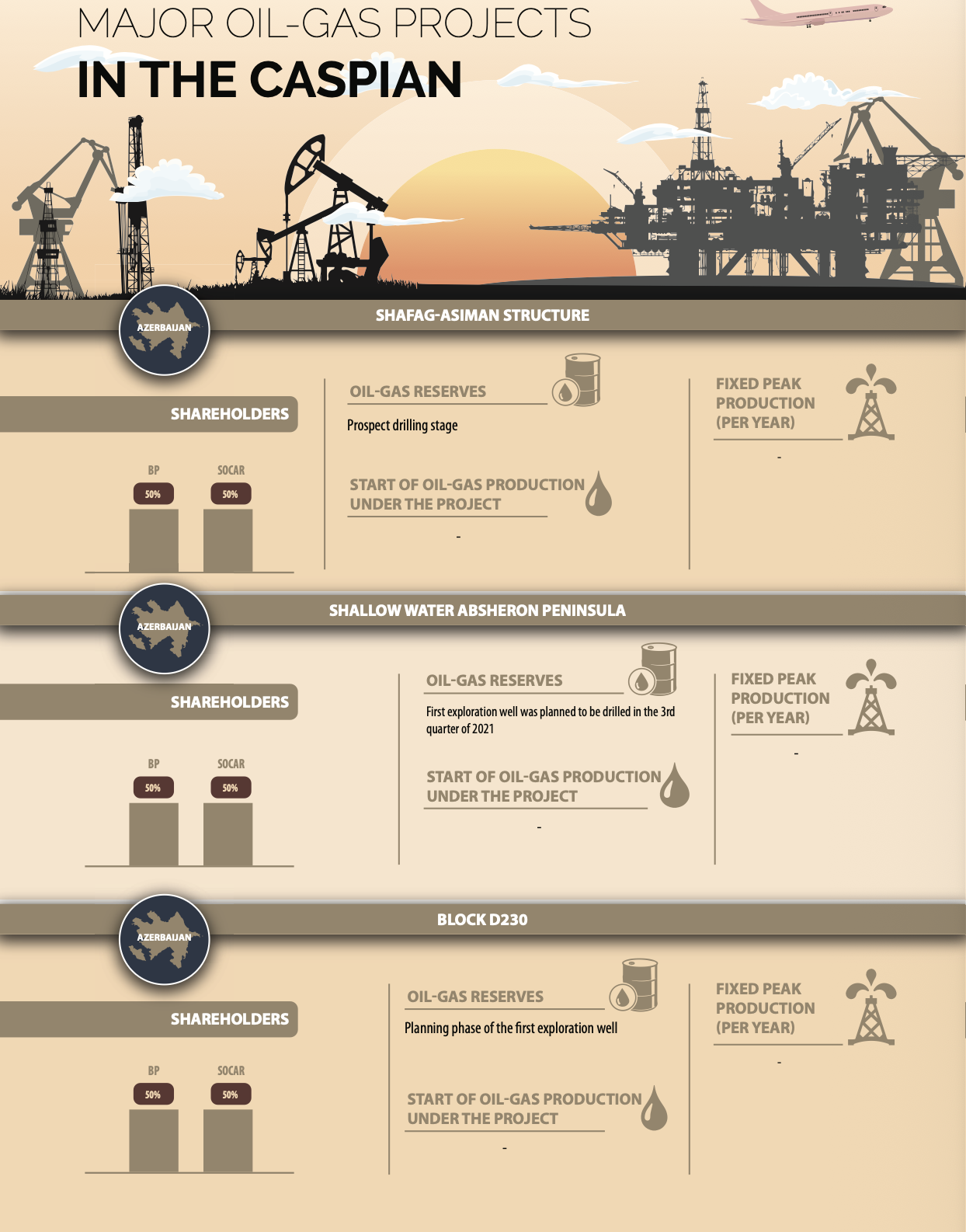

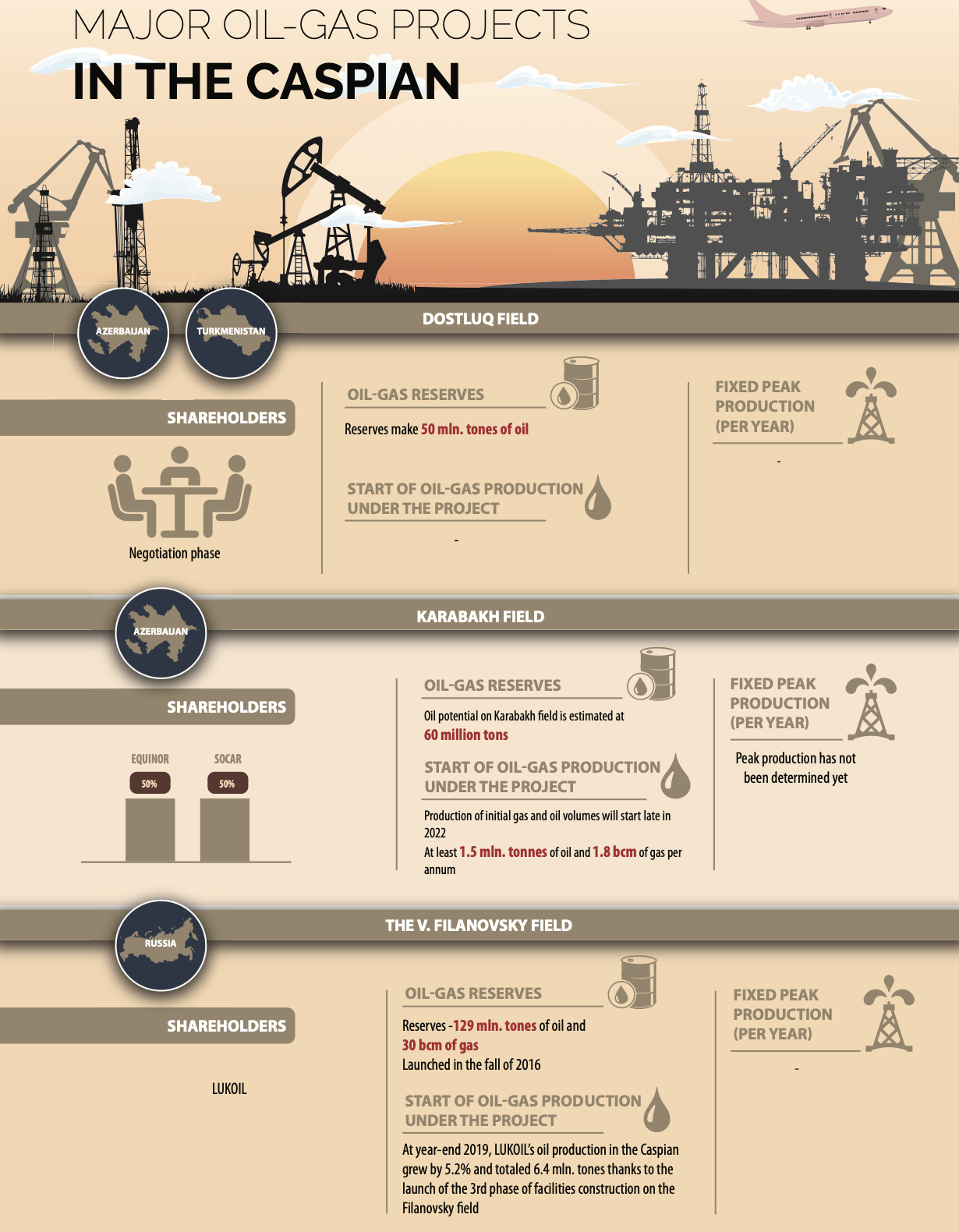

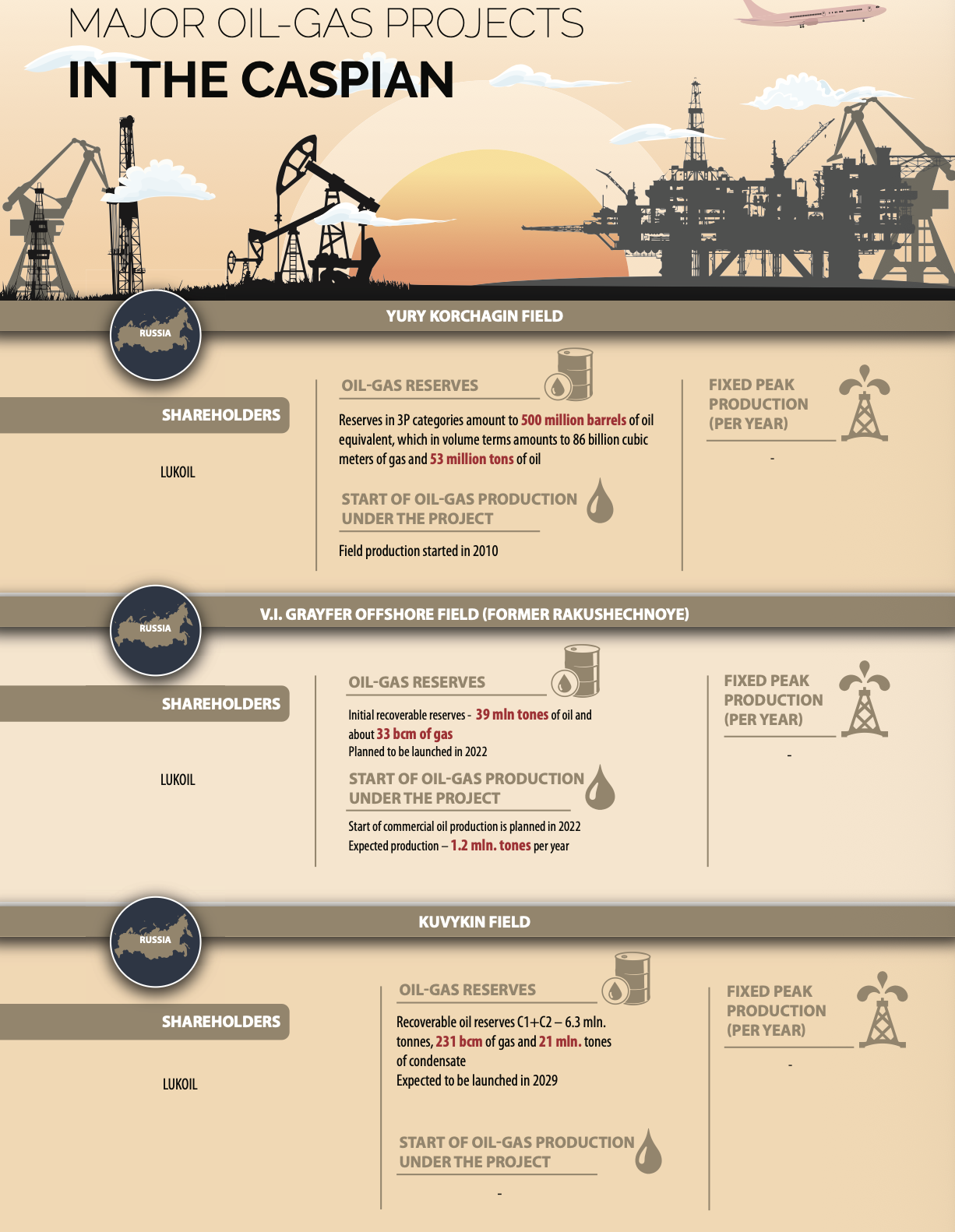

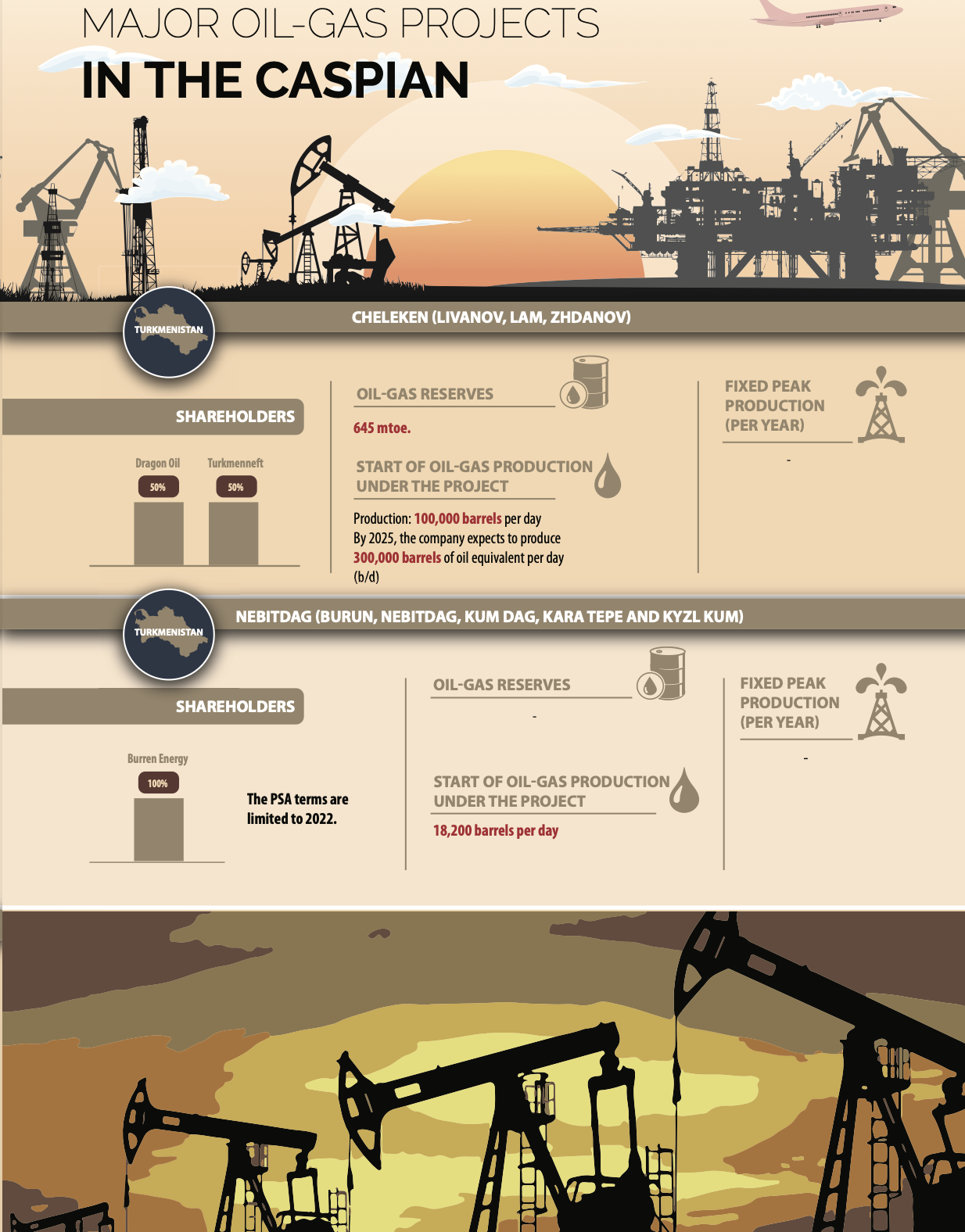

Considering environmental requirements and the European Commission’s recognition of natural gas as an official transitional energy resource, most of the focus is on gas production projects with reserves concentrated nowadays in the Azeri sector of the Caspian Sea. Despite its unpopularity, oil production is ongoing in the Caspian Sea, new fields are discovered and exploration is underway. The COP26 echoes are already heard in the Caspian, but are not yet visible, much less tangible. The highest percentage of equity participation belongs to LUKOIL, which has 100 percent in four Caspian projects. SOCAR and its traditional partner British bp are the undoubted leaders in terms of investment parameters, and Burren Energy is the most active in the Turkmen sector. In total, there are 17 active projects at various stages of development in the Caspian Sea, one of which was temporarily suspended in 2001. Commercial production is running on 9 fields. The most active work on exploration and delineation of new fields is underway in the middle part of the Caspian Sea - in the south-western part of the water body. In the northern part of the Caspian Sea, the most produced commodity is oil. KazMunaiGas and LUKOIL are the most active there.

The Azerbaijani National Company SOCAR, British bp and the American giant Exxonmobil are the leaders in terms of the volume of explored and under-development gas reserves. Then comes the Norwegian company Equinor followed by Turkish TPAO, Kazakhstani holding KazMunaiGas, American Chevron and French Total. Exxonmobil, Kazmunaigas, Shell and Agip (Kashagan shareholders), CNPC and Total possess the biggest volumes of oil assets in the Caspian Sea. Assets information is given below in the table.