")

")

The number of the Trans-Caspian gas pipeline (about 300km long) project related memoranda and declarations, which have been signed throughout this period including statements made for and against it, is probably higher compared to those of the Nabucco mega project.

However, it is the only common feature between them.

The project on linking the eastern and western shores of the Caspian Sea by a gas pipeline is indeed a visual reflection of practically all geopolitical processes, price crises, and indicates the importance of the Caspian in terms of the energy security of both Europe and Asian-Pacific region countries, the USA and Eastern Mediterranean countries.

There has been a glimmer in these processes as the EU and Turkmenistan now have a chance to unite their energy systems. The project anyway has a series of pro arguments.

The Trans-Caspian gas pipeline project has been under discussion since the beginning of the 90s of the past century. The consortium consisting of Amoco Corрoration, J.I.Caрital and Bechtel Enterрrises was formed in 1998 to implement a Trans-Caspian gas pipeline project, which implied conduction of engineering work, design, logistics operations and laying of the gas pipeline from the area close to the city of Turkmenbashi to Baku and further to Turkey via Georgia. A 1,738km long pipeline was expected to transport from 10 up to 35 bcm of gas per year. Earlier in 1997, the Royal-Dutch Shell had offered the similar project for export of Turkmen gas to Turkey by means of transit through Iran. However, the uncertainty about the Caspian Sea status hindered the implementation of that project.

It is noteworthy that another gas pipeline project (Peri-Caspian gas pipeline) was also destined to fail. In 2007, Presidents of Russia, Kazakhstan and Turkmenistan signed a declaration about construction of the Peri-Caspian gas pipeline which was going to increase the carrying capacity of a $2bln worth Central Asia – Center gas pipeline, heading to Russia, by 40 bcm – up to 80 bcm. Formerly, in 2003 Russian Gazprom signed a contract with Turkmengaz for purchase of Turkmen gas till 2028. However, after a technical problem that arose in April 2009 on the Russian-Uzbek section of Central Asia-Center-4 gas pipeline which used to supply Turkmen gas to RF, gas export fell by 80%. So, Turkmenistan promptly diversified its export to Iran and China and commissioned the first LNG terminal in the Caspian.

The Trans-Caspian gas pipeline is still on the agenda. “Gas distribution routes are being diversified all over the world and we also consider a European direction of export”, the Turkmen leader emphasized in 2007.

The EU has allocated 1.7 mln EUR for the feasibility study of Turkmenistan’s involvement in the Trans-Caspian gas pipeline project.

In October 2011, EU and Turkmenistan started working on creation of the contractual legal framework for supply of Turkmen energy resources in the European direction, President of Turkmenistan Gurbanguly Berdimuhamedov said during the negotiations with Federal President of Austria Heinz Fischer. In the same month, President of Russia Dmitry Medvedev held an unscheduled session of the Security Council where, as Rusenergy reports, he stated: “I would like to draw the attention of the Security Council members’ …to the issue concerning the construction of the Trans-Caspian gas pipeline along the bed of the Caspian Sea… The Russian Federation must consider its position in order to express it for our Caspian partners in case any certain decisions are being made”. Nothing is known about the decision made by the Security Council…, but the Trans-Caspian project was once again sidelined”.

In the fall of 2013 the EU raised an issue of implementation of the Trans-Caspian gas pipeline. However, “Our partners from the EU literally press the Trans-Caspian gas pipeline project on Azerbaijan and Turkmenistan, ignoring the fact that such issues should be solved by the Peri-Caspian states but not in Brussels”, RF Minister of Foreign Affairs Lavrov commented the project-related situation in one of his speeches.

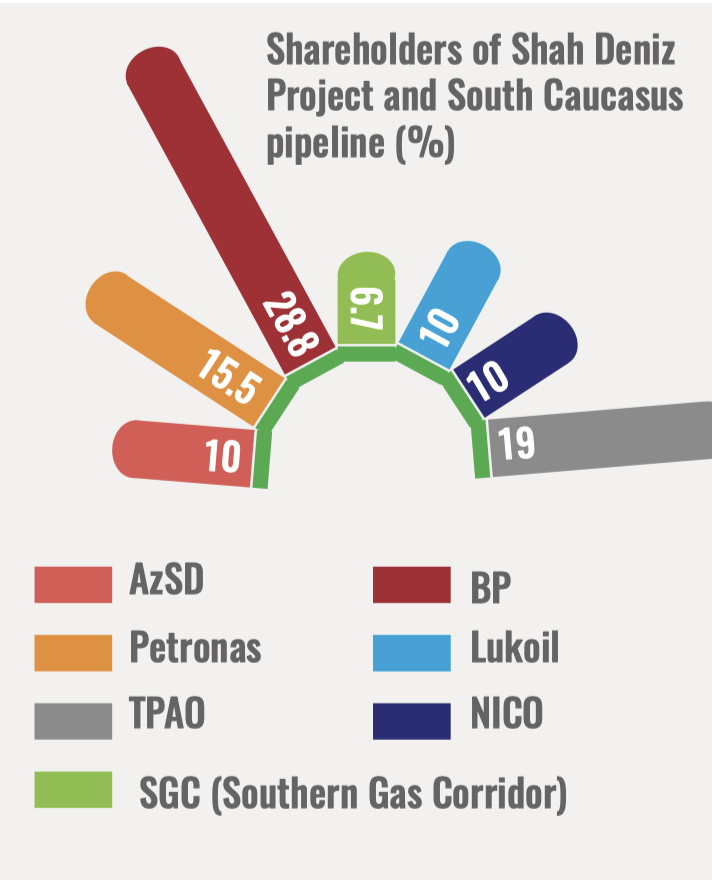

However, 2013 became a defining year for the whole Caspian region and especially for Azerbaijan, Caspian gas exporter to the European markets. In September SOCAR and Shah Deniz consortium signed export contracts worth altogether about $200 bln with 9 large oil-gas companies for yearly supply of approx 10 bcm for the 25-year period. Among those companies were Bulgargaz, Shell, Gas Natural Fenosa, DEPA, E.On, GDF Suez, HERA trading, Axpo and Enel.

The launch of Shah Deniz II gas production has been scheduled for 2019. However, gas volumes will have reached Europe in 2020. The production peak will be fixed in 2024 and last for 7-8 years.

The project is estimated at $40 bln. After the launch of Stage II of Shah Deniz field development, the total volume of gas extracted on the field is to increase up to 25 bcm. The reserves of Shah Deniz field are estimated at 1.2 trillion cubic meters of gas.

Late in June of 2013, the consortium for development of the Shah Deniz gas condensate field announced that it had chosen the Trans-Adriatic Pipeline (TAP) as a route for transportation of its gas to the European markets. The initial capacity of TAP will total 10 bcm per year with a potential for increase up to 20 bcm per year.

Later, another significant event took place at the Astrakhan summit in September of 2014 – for the first time the heads of 5 Caspian states reached a common consensus and settled major points of the convention on the Caspian Sea status. However, the practical delimitation of the seabed and subsoil of the Caspian Sea still remained outside the framework.

According to the Astrakhan statement of Presidents of Azerbaijan, Russia, Iran, Kazakhstan and Turkmenistan - “The activities of the parties on the Caspian Sea will be carried out on the basis of principles agreed by them, including national sovereignty of each side of the coastal maritime space within 15 nautical miles of the exclusive rights of each party for the production of aquatic biological resources within the adjacent 10 nautical miles, followed by the common water space, with the understanding that the issue of the application of techniques with establishment of baselines will be the subject of further consultations between the parties”. The document also enshrines the principles of “delimitation of the seabed and subsoil of the Caspian Sea on the basis of universally recognized principles and norms of international law in order to implement the sovereign rights of the parties on the use of mineral resources and other legitimate economic and business activities related to the development of the seabed and subsoil resources by agreement of the parties.”

“Azerbaijan has been implementing an energy policy for already 21 years, starting from 1994, when we began working on development of large oil fields of our country. At that time several oil pipelines were built in order to transport resources to the world markets as we have no access to the world oceans. Gas reserves were discovered late in 90s. Since then we have started working actively to produce gas, and have already producing it in certain volumes starting from 2007. We already supply inconsiderable volumes of gas to our neighbors – Turkey, Georgia, Iran, and at the same time to Russia. Reserves that we possess are very big. Therefore, we certainly should sell them”, President of Azerbaijan Ilham Aliyev said in his interview with the Russian TV channel in April of this year.

Besides, “…gas revenues are not comparable with those of oil. Oil export, which has been currently stabilized, still remains the main source of currency earnings, it is the way it is going to be for a long period. Gas factor will certainly strengthen our economy and considerably raise Azerbaijan’s role and the country’s significance for consumers. Every country wants its role and significance to grow. Thereby, our potential will be able to grow as well”, I.Aliyev noted.

“The Southern Gas Corridor” project implies the development of the Shah Deniz II project. 16 bcm of gas are annually expected to be produced and sold within the framework of this project in addition to 8 bcm that we are already selling. Of this volume, 6 bcm will flow to Turkey. 10 bcm will be delivered to several European countries”, President concluded.

Thus, sale of own reserves and energy resources on the global markets is a major priority for Azerbaijan. Besides, increased geopolitical risks, market uncertainty, suddenly appeared parallel gas pipelines, different types of restrictive factors on the final markets, disadvantage gas projects compared with the oil export. Though, it is worth mentioning that starting from 1994 until July 13, 2006 (commissioning ceremony of the Baku-Tbilisi-Ceyhan system) Azerbaijan had to face similar problems while implementing its oil strategy. However, plain, clear and open position of Baku will help to overcome them even today. By 2020, big gas reserves (over 2.5 trillion cubic meters of recoverable reserves) along with a developed infrastructure will have ensured high competitiveness of Azerbaijani gas at any markets for coming 30 years.

EU makes it clear that it does not intend to give up the implementation of the Trans-Caspian gas pipeline project, but is not willing to make any contributions to it, like with Nabucco. In April 2015 the European Commission once again offered Azerbaijan and Turkmenistan to update a memorandum of understanding (dated 2011) for construction of the Trans-Caspian gas pipeline.

“We see Turkmenistan’s growing interest in development of relations in this area”, Vice President of the European Commission M. Šefčovič noted. “We are considering several opportunities in order to make sure that we will have more options and obtain the best result for Europe during negotiations we are going to hold in the global market”, the representative of the EU management said.

On May 1, Ashgabat hosted the meeting of the ministers of energy of Turkmenistan, Azerbaijan, Turkey and the EU.

The Ashgabat meeting resulted with the following decision:

- to systematically continue 4-sided negotiations,

- to negotiate prospects of creation of Corporation for gas supply to EU,

-to start consulting with global gas companies in order to determine effective structure of the Corporation,

- to create a working group for operative addressing of issues,

- to negotiate commercial success of long-term gas supplies from Turkmenistan to Europe,

- to initial declaration at the end of the meeting.

Commenting the results of the meeting within the framework of the session of the Caspian European Club, Minister of Energy of Azerbaijan Natig Aliyev said that in near future the parties will inform each other about the members of the working group.

“I think that representatives of the ministries of energy, justice, foreign affairs as well as the State Oil Company of Azerbaijan Republic (SOCAR) will represent the Azerbaijani side within the working group”, N.Aliyev said.

At the same time, N.Aliyev spoke about the idea to create a so called “Caspian consortium” which shall consist of authoritative energy companies of Europe.

“They also will be customers of gas. Apart from this, all issues concerning even the construction of the trans-Caspian gas pipeline could be solved within the framework of the consortium.

However, It is not completely clear yet. Moreover, solution of these issues will take time. The negotiations are ongoing”, the head of the ministry said.

Turkmenistan is now completing the construction of the East-West gas pipeline which will combine major gas fields of Turkmenistan into the single gas transportation system and will enable to considerably increase the export of the country, President G.Berdimuhamedov said during his official visit to Viena from May 11 to 13. “Construction of this gas pipeline, capable of delivering in the long-term big volumes of Turkmen energy resources in the required direction, will provide an additional guarantee for their reliable and stable export”, G.Berdimuhamedov emphasized.

It was reported late in March that Turkmenistan is testing the East-West export gas pipeline. The carrying capacity of the new regional 773km long gas pipeline, laid from Shatlyk to Belek, totals 30 bcm per year. Gas pipelines, which will be interconnected with Dovletabat-Daryalik, Shatlik-Abadan, Bami-Serdar, Central Asia-Center gas mains, are under construction. A ground for construction of the new Compressor Station Shatlyk is being prepared. The country’s largest field Galkynysh will be a main feedstock source for the East-West gas pipeline.

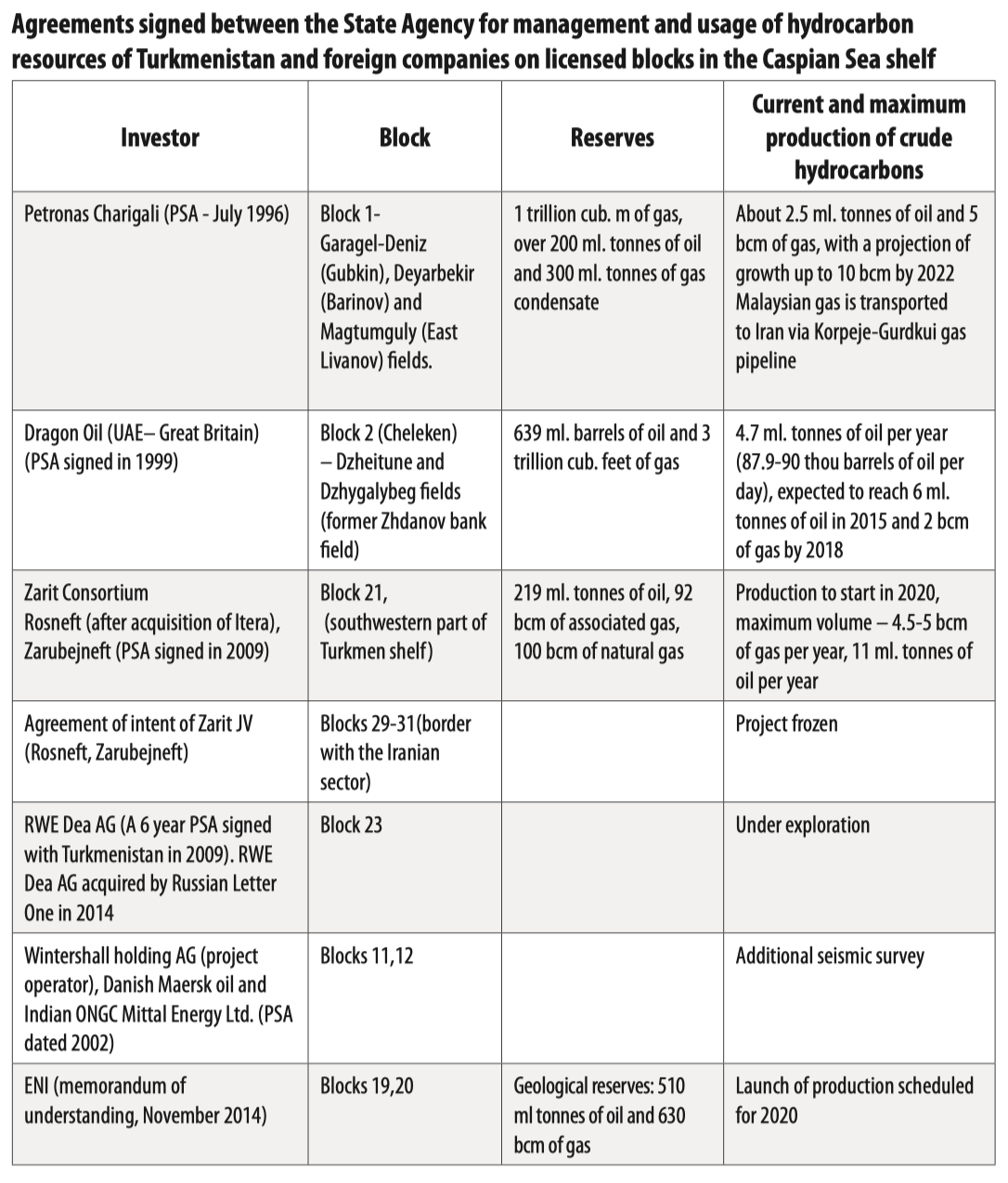

The head of Turkmenistan also noted that in addition to available onshore fields, the country possesses sufficient energy reserves in the Turkmen sector of the Caspian Sea to meet the volumes of the European projects. As early as 2000s, the government of Turkmenistan allocated 32 blocks in the Turkmen sector of the Caspian Sea to sign PSA with foreign investors for exploration and development of oil-gas fields. Malaysian Company Petronas Charigali, implementing the Block I project, shall become a major gas producer on the shelf. The block includes Diyarbekir (Barinov), Garagol-Deniz (Gubkin), Magtumguli (Eastern Livanov) and Ovez (Central Livanov) fields. Commercial production of oil and its export have been launched since May 2006. The annual production currently exceeds 2 mln tonnes. Export is carried out by means of the Baku-Tbilisi-Ceyhan (BTC) system. Petronas has considerably increased its assets in the Caspian after closing a deal with the Norwegian Statoil late in April of this year on acquisition of a 15.5% stake in the Shah Deniz project.

Apart from this, the Malaysian company marked the export direction of the Block -1 (Turkmen shelf) via the Southern Gas Corridor as Petronas also bought a 15.5% stake in the Southern Gas Corridor project (South Caucasus Pipeline Company, SCPC) and a 12.4% stake in AGSC (Azerbaijan Gas Supply Company). The sum of the deal makes $2.25 bln.

Turkmennebit started developing a shallow part of the Caspian Sea about three years ago. “Oilmen have recently completed prospecting and exploration work on wells # 201, 202 and 204. As a result, each well started producing on average 50-60 tonnes of oil per day. These developed new productive oil-prone formations indicated prospectivity of the water shelf of North Goturdepe field”, says the ministry of oil-gas industry and mineral resources of Turkmenistan. Earlier it was reported that hydrocarbon resources of the Turkmen shelf are estimated at 12 bln tonnes of oil and 6.5 trillion cubic meters of gas. A number of contract areas located at medium and high depth were put up for an international tender.

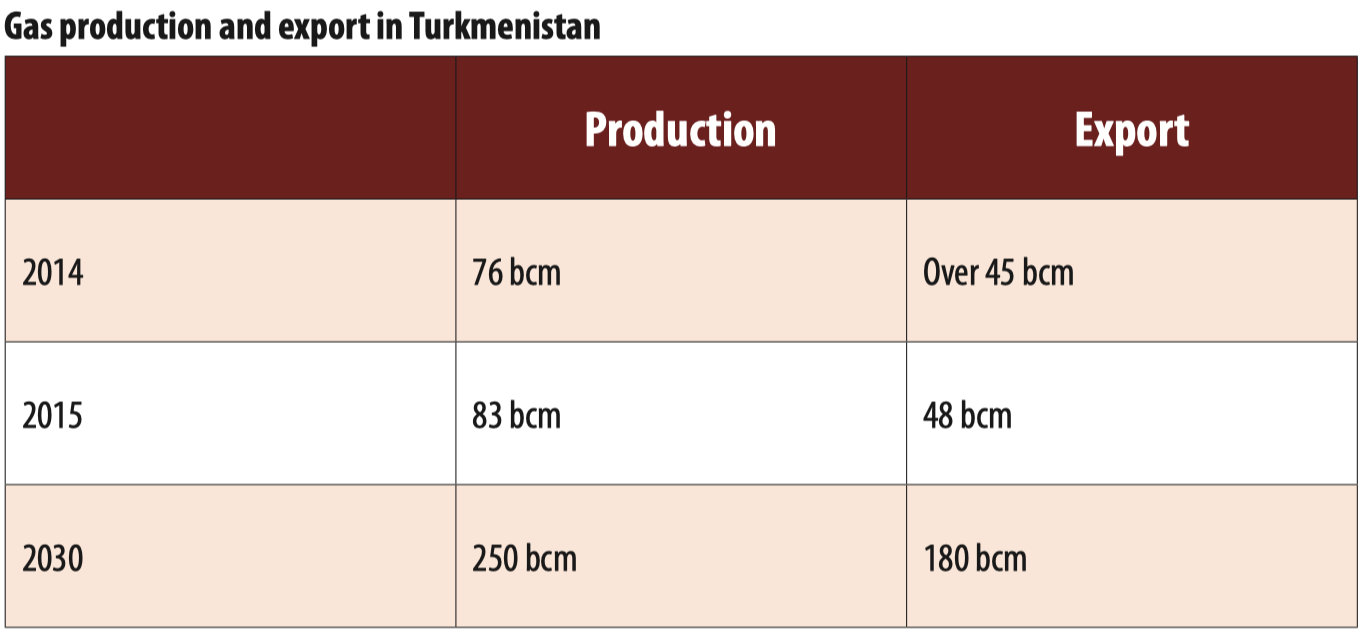

Addressing the enlarged session of the government, dedicated to the results of 2014, President of Turkmenistan Gurbanguly Berdimuhamedov noted that in 2015 Turkmenistan’s FEC has to increase natural gas production by 9% (up to 83.8 bcm) and its export up to 48 bcm.

Russian companies, namely Rosneft, have been intentionally expanding their presence in the Caspian for the last 3 years. Acquisition of 100% shares of TNK-BP Ltd. by Rosneft late in 2012, which made BP (major investor of Caspian projects of Azerbaijan) an owner of a 19.75% stake in the Russian Company, had an impact on the Caspian in 2014. Alfa-Group spent means gained from sale of TNK-BP on purchase of the German Company RWE Dea AG (see the table) via own investment company Letter One for 5.1 bln EUR. It is noteworthy that the German company has a license for exploration and development of one of the major gas blocks of the Turkmen shelf in the Caspian.

Formerly Rosneft bought Russian Itera, one of the major assets of which were blocks of gas structures in the southern part of the Turkmen sector (see the table).

In May 2014, Rosneft and Azerbaijani SOCAR signed an agreement on establishment of the joint venture in regard to the projects on oil-gas production and exploration in sectors that are under different jurisdictions, including in Azerbaijan and Russia. In spite of the fact that the list of assets will be agreed additionally, the frames of cooperation of the two state companies, including in the Caspian, have already been determined. As the Russian Gazprom is a monopolist of gas export within Russia as well as manages all four branches of the Central Asia-Center gas pipeline, it is most likely that Rosneft will represent RF both in international upstream and midstream projects. In other words, Rosneft can show up at any time as one of the major investors into large transboundary fields in the Caspian (for instance, Zarit block of gas condensate structures, large oil field Kapaz (Serdar), a big block of gas condensate structures Araz-Alov-Sharg) and as a member of the International Consortium for construction of the Trans-Caspian gas pipeline from Turkmenistan to EU, which is being formed together with Petronas, ENI and other investors of the Caspian shelf of Turkmenistan.

Turkmenistan expresses discontent in cooperation with Gazprom. In particular, in 2015 Russia “once again groundlessly stated about lowering the volume of purchased Turkmen gas from 11 bcm down to 4 bcm per year”, says the article of Deputy Director of the Oil and Gas Institute of the State Company Turkmengaz Annadurdi Meretgeldiyev, published at the governmental website of Turkmenistan in February 2015. Russia and Gazprom assumed obligations to invest in Turkmenistan into the construction of the Peri-Caspian gas pipeline and East-West gas pipeline. However, they failed to fulfill their obligations, he notes. It shows that “the biggest energy company is not a stable partner”.

Caspian projects of Rosneft can strengthen positions of this company at global markets as the Russian government is nowadays taking stimulating measures for activating geological exploration and discovering new fields, fearing the decline of oil-gas production after 2020. Rosneft can start commissioning its south assets amid the delay of performance of operations at ten sites of the Arctic shelf. According to Vice President of Rosneft Mikhail Leontyev, here in the considerable part of the East-Siberian Sea there was practically no ice-free water area over the past 15 years. Moreover, for now there are no technologies for performing operations on ice or below it”.

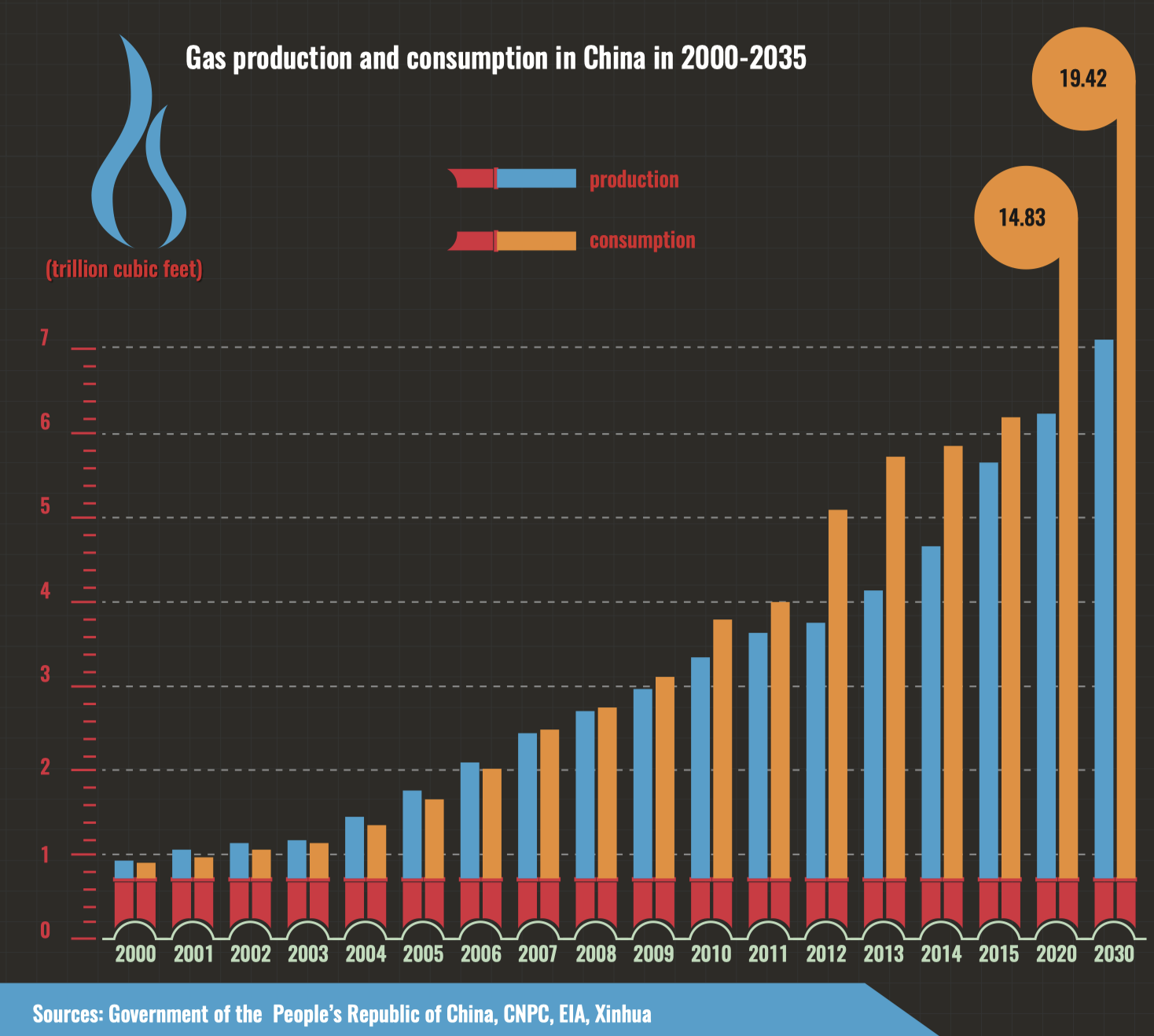

Apart from this, diversion of Turkmen export from the priority Chinese direction will enable to strengthen Gazprom’s positions in China as far as possible. Gazprom and CNPC signed an agreement on purchase-sale of natural gas and its supply along the eastern route in May 2014. The cost of a 30-year contract is $400bln. The first gas supplies will be commenced in 2019 along the underconstruction gas pipeline “Sila Sibiri”. The peak of supplies will total 38 bcm per year after 2022.

In spite of the fact that neighboring China is a direct and natural market for Turkmen gas, diversification of routes is the way for Ashgabat to influence on the pricing environment of its gas export.

Almost 80% of Turkmenistan’s state budget is aimed at gas export revenues. Demand in China will have been increased almost twice as much by 2020 (350 bcm per year). Domestic production of China will cover about 115 bcm. Another 80 bcm will fall to the share of LNG supplies. Supplies from the Asian-Pacific region countries will not exceed 40 bcm. According to forecasts of global experts, gas consumption in China will surpass the European one by 2020, which now totals about 600 bcm.

In 2007, CNPC was the only one among foreign companies which signed PSA with Turkmenistan on onshore field Bahtiyarlik containing big gas reserves (1.3 trillion cubic meters). This project is a major gas source for supply along the Turkmenistan-China (13 bcm in 2012) pipeline. Chinese companies are working on the field.

In 2009, the state company Turkmengaz signed a credit agreement worth $4bln with the state China Development Bank in order to finance operations on the giant Galkynysh field where reserves reach up to 21 trillion cubic meters of gas (former South Eloten-Osman).

A and B branch lines of Central Asia–China gas pipeline were commissioned late in 2009 and October 2010 respectively.

In 2011, China allocated another $4.1 bln to Turkmengaz for the same purposes. Apart from this, an agreement about multilateral cooperation was signed between SC Turkmengaz, PetroChina (subsidiary of CNPC) and state China Development Bank, stipulating guarantees of credit repayment at the expense of supply of Turkmen gas.

A new contract for supply of 25 bcm of gas per year was signed with Peking in September 2013 when Head of the People’s Republic of China Xi Jinping paid a visit to Ashgabat. As a result, China will purchase 65 bcm from Turkmenistan. A new contract was timed to coincide with the solemn commissioning ceremony of Galkynysh field due on September 4. The second phase of development of Galkynysh with the production volume of 30 bcm will be a resource base for a new contract. China Development Bank will ensure financing of the project via a tied credit.

The third branch line (C) of the Central Asia-China gas pipeline was launched in June 2014. According to the report of CNPC, the C branch has been laid parallel to A and B branch lines of the gas pipeline. Its total length makes 1,830km. Besides, the projected carrying capacity of the C branch line totals 25 bcm per year of which 10 bcm will flow from Turkmenistan, 10 bcm from Uzbekistan and 5 bcm from Kazakhstan.

According to the report, the C branch line starts on the border f Turkmenistan and Uzbekistan, crosses through Kazakhstan and ends in Xinjiang Uygur Autonomous Region of China, where it gets linked to the third line of the domestic West-East Chinese gas pipeline. The construction of the C branch line started in September 2012.

In 2014, the National Holding Company Uzbekneftegaz and Chinese National Petroleum Corporation (CNPC) signed an agreement of intent to create the second JV for the construction and operation of the gas pipeline. The need for creation of the second JV has been associated with the project financing issues. The construction of the Uzbek section of the fourth line of the Central Asia-China gas pipeline will start in mid of 2015.

In general, the fourth line of the Central Asia-China gas pipeline with the total length of about 1,000 km will cross through the area of 5 countries – Turkmenistan, Uzbekistan, Tajikistan, Kyrgyzstan and China – and will let increase increase total carrying capacity up to 85 bcm.

Beyond a shadow of doubt, the China’s positions have become too strong to be ignored. At the same time China, playing on the weak strings of the “run-of-the-mill European energy policy” in the region, has already frozen out European investors from the onshore fields in Turkmenistan and now it is the Caspian Sea’s turn. Taking into consideration the strategic alliance between Russia and China, which has come into being for different reasons, including the European policy, the EU has concerns to worry about. It may lose Caspian gas at all. If the EU loses the Trans-Caspian after Nabucco, it can lose not only the Turkmen shelf, but the entire Caspian Sea. And that is what actually happening now, swiftly and silently, to the accompaniment of loud statements of the West.